When you pick up a prescription, have you ever wondered why one pill costs $6 and another, with the same name and same effect, costs $60? The answer isn’t about quality, effectiveness, or safety. It’s about generic medications-and how they cut costs across the entire healthcare system.

Same Drug, Lower Price

Generic drugs are not knock-offs. They’re not inferior. They’re exact copies of brand-name medications in every way that matters: same active ingredient, same dose, same way it’s taken, same strength, same shelf life. The FDA requires them to work the same way in your body. If your doctor prescribes Lipitor for cholesterol, and you get atorvastatin instead, you’re getting the same medicine-just without the brand name.

So why the price difference? Because brand-name companies spent years and hundreds of millions of dollars developing the drug. They ran clinical trials, tested side effects, proved it worked, and paid for marketing. Once the patent runs out-usually after 12 to 15 years-any manufacturer can make the same drug. And when they do, prices drop fast.

How Competition Drives Prices Down

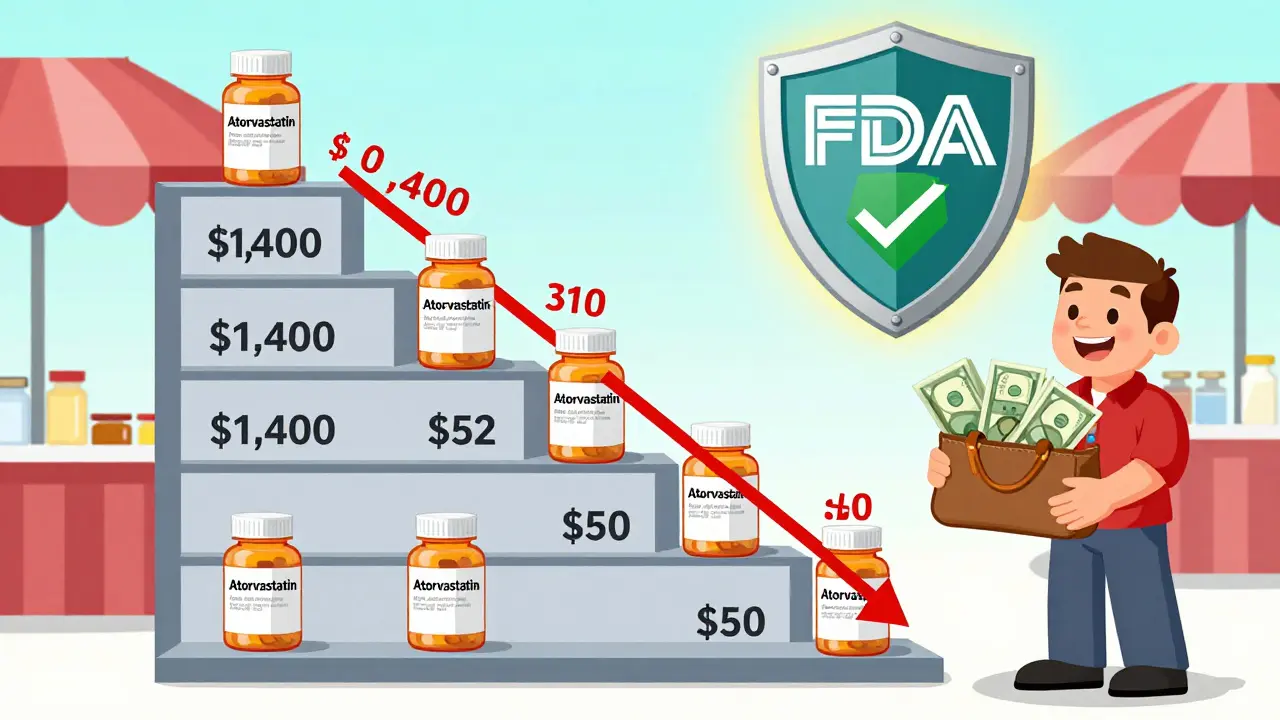

The moment a generic enters the market, the price begins to fall. One generic? The drug might cost 30% less. Two generics? Down another 20%. By the time five or six companies are making it, the price often drops to just 15% of the original brand-name cost. The FDA found that in markets with three or more generic manufacturers, prices fall by about 20% every year after the first generic arrives.

Take lurasidone, a drug used for schizophrenia. When it was brand-name (Latuda), a 30-day supply cost around $1,400. After generics hit the market, that same dose dropped to under $60. That’s a 95% price drop. Another example: pemetrexed (Alimta), used for lung cancer. The brand version cost nearly $3,800 a month. Generics brought it down to about $500. That’s $3,300 saved per patient, every month.

These aren’t rare cases. In 2022 alone, generic and biosimilar drugs saved the U.S. healthcare system over $408 billion. Over the last decade, that total hits $2.9 trillion. That’s not just money saved-it’s lives made affordable.

Why Insurers Love Generics

Insurance companies don’t pay the full price of a drug. They negotiate discounts, but they still pay a lot. A brand-name drug might cost $100 per prescription. A generic? Maybe $6. That’s a 94% reduction in cost for the insurer. And since insurers cover millions of prescriptions each year, those savings add up fast.

That’s why most insurance plans have tiered formularies. Generics are usually in Tier 1-the cheapest. Brand-name drugs? Tier 3 or 4, with much higher copays. In 2023, the average copay for a generic was $6.16. For a brand-name drug? $56.12. Nearly nine times more.

And here’s the kicker: 93% of all generic prescriptions cost less than $20. Only 59% of brand-name prescriptions do. That’s why insurers push generics-they’re not just cheaper for patients, they’re cheaper for the whole system.

Not All Generics Are Created Equal

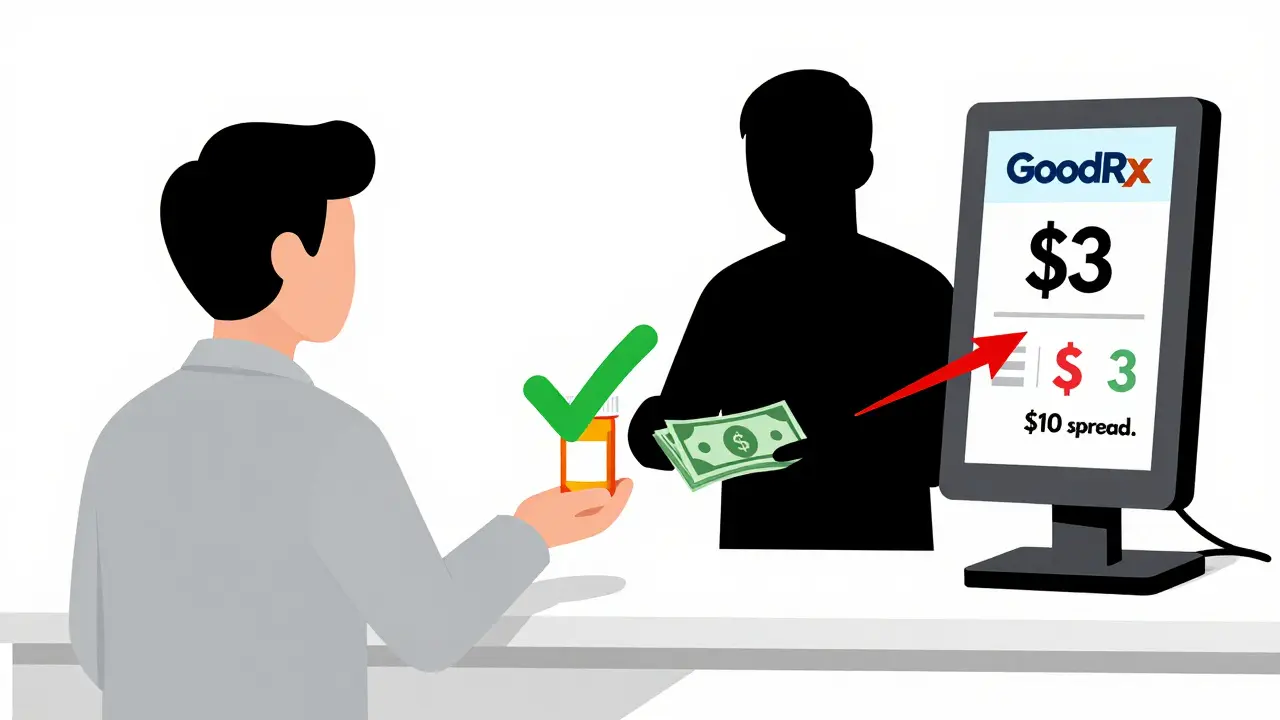

Here’s where things get tricky. Not every generic is cheap. Some generics cost almost as much as the brand-name version. Why? Because of how pharmacy benefit managers (PBMs) work.

PBMs are middlemen between insurers, pharmacies, and drug makers. They negotiate prices. But some use a practice called “spread pricing.” They tell the insurer they paid $10 for a drug, but they actually paid $5. They pocket the $5 difference. That’s fine if the drug is cheap. But if the generic is priced at $40, and the PBM negotiates $30 from the manufacturer, they still make $10 profit-even if a cheaper version exists for $10.

A 2022 study in JAMA Network Open found 45 generic drugs that were 15 times more expensive than other, equally effective alternatives. In Colorado, replacing just those high-cost generics would have saved $6.6 million. That’s money taken from patients’ pockets and given to middlemen.

This isn’t about the drug. It’s about the system. A generic isn’t automatically cheap. Sometimes, you need to look beyond the label.

How to Save Even More

You don’t have to accept whatever price your pharmacy gives you. Here’s how to find the real deal:

- Ask your doctor to write “dispense as written” on your prescription. That gives your pharmacist the legal right to swap in a generic if one is available.

- Use free price-comparison tools like GoodRx or SingleCare. They show cash prices at nearby pharmacies-often cheaper than your insurance copay.

- Try mail-order pharmacies for maintenance drugs (like blood pressure or diabetes meds). They often offer 90-day supplies at lower rates.

- If you’re uninsured, consider the Mark Cuban Cost Plus Drug Company. It sells generics at cost plus a small fee. One study found it saved users $4.96 per prescription on average.

Patients who actively compared prices saved an average of $287 a year. That’s not a lot of effort-just five to seven minutes per prescription.

What About Quality and Safety?

Some people worry generics aren’t as safe. They’re not. The FDA requires generics to meet the same strict standards as brand-name drugs: same purity, same strength, same stability. They’re tested in labs. They’re inspected in factories. The FDA approves 600-700 new generic drugs every year. That’s not luck. That’s oversight.

Even the FDA says: “Generic drugs are just as safe and effective as brand-name drugs.” If your brand-name drug works, the generic will too. No exceptions.

The Bigger Picture

Generics aren’t just about saving money. They’re about access. A cancer patient who can’t afford $4,000 a month for Alimta might skip doses-or skip treatment entirely. With a generic at $500, they can keep taking it. A diabetic who pays $100 for insulin instead of $15 can manage their condition without choosing between medicine and rent.

And it’s getting better. More biologic drugs-expensive, complex treatments for conditions like rheumatoid arthritis and multiple sclerosis-are losing patents. Biosimilars, the generic version of biologics, are coming. IQVIA estimates they’ll save $150 billion between 2023 and 2027.

But challenges remain. Some generic drugs are at risk of shortage. If only one company makes a drug, and they have a production problem, prices spike. The FDA tracks over 200 “at-risk” generics. That’s why competition matters more than ever.

Final Thought: Ask, Compare, Save

Generic drugs are one of the most powerful tools we have to make healthcare affordable. They’re safe. They’re effective. And they’re often dramatically cheaper. But you have to know how to use them.

Don’t assume your insurance will always get you the best price. Don’t assume the pharmacy will tell you about cheaper options. Take five minutes. Compare prices. Ask your pharmacist. Switch if you can. You’re not just saving money-you’re making sure you can keep taking the medicine you need.

Are generic drugs as safe as brand-name drugs?

Yes. The FDA requires generic drugs to have the same active ingredients, strength, dosage form, and quality as brand-name drugs. They must also meet the same strict manufacturing standards. Generics are tested for bioequivalence-meaning they work the same way in your body. Millions of people use generics safely every day.

Why do some generic drugs cost more than others?

Not all generics are priced the same. Some are expensive because only one company makes them, or because pharmacy benefit managers (PBMs) use spread pricing to profit from the difference between what they pay and what they charge. In some cases, a generic drug might cost more than a cheaper alternative with the same effect. Always compare prices using tools like GoodRx to find the best deal.

Can I save money by buying generics without insurance?

Yes, sometimes. Many uninsured patients find that cash prices at pharmacies using discount apps like GoodRx or the Mark Cuban Cost Plus Drug Company are lower than their insurance copay-especially with high-deductible plans. One study showed cash purchases saved users an average of $4.96 per prescription. Always check both options.

Do insurance companies prefer generics?

Absolutely. Generics cost insurers far less than brand-name drugs. Most plans put generics in the lowest copay tier, often $5-$10, while brand-name drugs can cost $40-$100. Insurers encourage generics because they reduce overall spending, which helps keep premiums lower for everyone.

What should I do if my generic isn’t working like the brand?

If you notice a change in how a medication works-like side effects or reduced effectiveness-talk to your doctor. While rare, some people may react differently to inactive ingredients (like fillers) in generics. Your doctor can switch you to a different generic manufacturer or, if needed, prescribe the brand-name version. Always report changes to your healthcare provider.

John Smith

February 26, 2026 AT 04:48Meanwhile, the real scam is PBMs pocketing the difference while you're told to 'be grateful' for savings that never reach you

Shalini Gautam

February 27, 2026 AT 05:00My aunt took a generic for hypertension and paid ₹15 instead of ₹1500

Same pill, same effect, no drama

Why should Americans pay 10x more just because they don't ask?

Natanya Green

February 28, 2026 AT 06:19AND THE FACT THAT SOME GENERIC DRUGS COST MORE THAN THE BRAND?!?!

AND PBMs are just... stealing?!?!

MY MIND IS BLOWN!!!

I'M GOING TO CALL MY PHARMACY RIGHT NOW AND DEMAND A PRICE BREAKDOWN!!!

THIS IS THE MOST IMPORTANT THING I'VE LEARNED SINCE I FOUND OUT AVOCADOS AREN'T A FRUIT!!!

Holley T

March 1, 2026 AT 21:31Ashley Johnson

March 2, 2026 AT 01:53Big Pharma owns the FDA

They let generics in so they can control the market

They pick which companies get to make the generic

Then those companies pay bribes to PBMs

And your insulin? It's not that it's expensive

It's that they're making sure you can't get the cheap one

They want you dependent

They want you scared

They want you paying

And they're laughing all the way to the bank

tia novialiswati

March 3, 2026 AT 09:59So proud of you for sharing this!! 🎉

Seriously, this info could save someone's life!! 🙌

Don't forget to use GoodRx - it's like magic for your wallet!! ✨

And if you're uninsured, Mark Cuban's place is a GIFT!! 🎁

You're helping people!! I'm cheering for you!! 🥳

Christopher Brown

March 4, 2026 AT 20:10Stop blaming PBMs

Stop blaming insurers

Stop waiting for someone to fix it for you

Go to a pharmacy. Ask for cash price. Buy the cheapest one

It's not complicated

It's not a conspiracy

It's your responsibility

Kenzie Goode

March 6, 2026 AT 16:25It's not just about money

It's about how broken the trust is between patients, doctors, pharmacies, and insurers

We're all stuck in this cycle of assuming the system works

When really, we're just guessing what's fair

And nobody's asking the right questions

Like... who really benefits when we don't ask?

Dominic Punch

March 7, 2026 AT 00:09Let me tell you - the system is designed to confuse you

Generics aren't inherently cheap - they're only cheap when competition is real

But here's the kicker: if you ask your pharmacist for the lowest cash price - not the insurance price - they'll often show you a generic that's 80% cheaper than what your copay says

And yes, it's legal

And yes, they're not required to tell you

So do it yourself

Check GoodRx

Ask for the cash price

Don't wait for permission

You're worth the effort